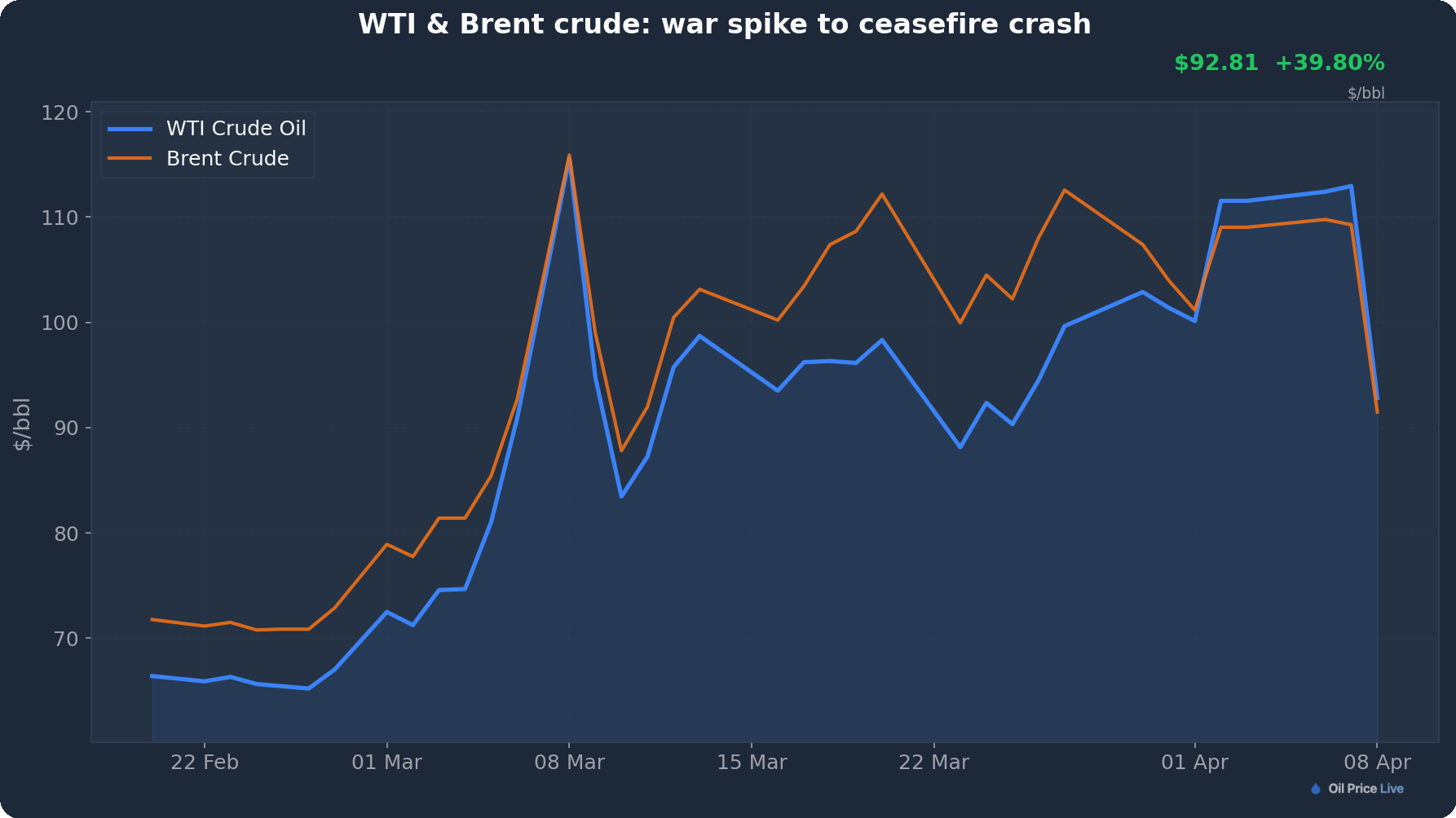

WTI crude fell below $93 on Wednesday afternoon, down roughly 20% from Tuesday's close near $116. Brent dropped under $92. The ceasefire between Washington and Tehran lit the fuse, but the sell-off has kept accelerating through the session. At least five distinct forces are at work.

1. Ships are moving through Hormuz

The truce alone wasn't enough to crater prices this far. What tipped the balance on Wednesday was confirmation that the first commercial vessels had begun transiting the Strait of Hormuz under Iranian escort. With 426 tankers and 34 LPG carriers queued up to leave the Gulf, each ship that clears the chokepoint makes the reopening feel less like a promise and more like a fact. The risk premium evaporates barrel by barrel.

2. Hedge funds are dumping long positions

Five weeks of war pushed speculative money into crude at a furious pace. Traders built massive long positions betting that Hormuz would stay shut and prices would keep climbing. Those bets are unwinding fast. Stop-losses and margin calls are forcing liquidation, each wave of selling drags the price lower, which triggers more stops. Bloomberg and Hedgeweek both reported that popular oil longs have been liquidated across major commodity desks this week, with quant funds and CTAs hit especially hard. That self-reinforcing loop has added momentum all day.

3. Four hundred million barrels of SPR crude still flowing

In mid-March, the US released 172 million barrels from the Strategic Petroleum Reserve as part of a coordinated move by 32 IEA member nations that totaled 400 million barrels. The flood was designed to cushion a wartime supply shock. But the crisis may be fading while the barrels aren't. They're entering the market on a schedule that won't reverse overnight, adding supply at exactly the moment demand for emergency crude is vanishing.

4. Wall Street is pricing in a recession

Goldman Sachs on April 6 raised US recession odds to 45% over the next twelve months and slashed its 2026 Brent forecast to $58 a barrel. JP Morgan pegs Brent at $68 and WTI at $65 for the full year. Both banks see global demand growing by roughly 0.9 million barrels per day, well below the pace needed to absorb current production. Five weeks of $100-plus oil acted as a tax on consumers and businesses. That economic damage doesn't reverse just because prices are falling.

5. The pre-war glut is waiting underneath

Before a single bomb fell on February 28, the oil market was headed for trouble. Crude started the year at $61. The IEA had flagged a surplus of up to 4 million barrels per day for 2026, the largest annual oversupply on record. OPEC+ members have been sitting on millions of barrels of voluntary production cuts and have already started unwinding them with a 206,000 bpd increase for May. Non-OPEC supply from the US, Brazil, and Guyana keeps growing regardless of what happens in the Middle East.

Strip out the war premium and the banks' base-case models land somewhere between $55 and $70. Below $93 already, there may still be a long way down.

What to watch next

The EIA weekly petroleum report, due at 10:30 AM ET today, could add fuel if inventories show a build. Beyond that, the ceasefire expires on April 22, and any sign it might collapse would reverse the trade instantly. For now, momentum belongs to the sellers.